$BWEN: GE Vernova Is Sold Out Through 2030. This Is Theirs and Siemens Machining Partner.

Power Generation · May 2026

AI Is Power Hungry

Power demand in the US has hit a level nobody in this industry was prepared for. The culprit is obvious: AI data centers are pulling electricity at a scale that has completely overwhelmed grid planning models built for a different era. Hyperscalers are signing PPAs for gigawatts they need delivered yesterday, and utilities are scrambling to source generation fast enough to keep up.

The solution the market landed on is gas turbines. Not because they’re perfect, but because they’re the only dispatchable generation technology that can be permitted, financed, and built fast enough to matter. Solar and wind are great, but they’re not firm power. Batteries help at the margin. Gas turbines are what you reach for when you need guaranteed megawatts on a timeline measured in months.

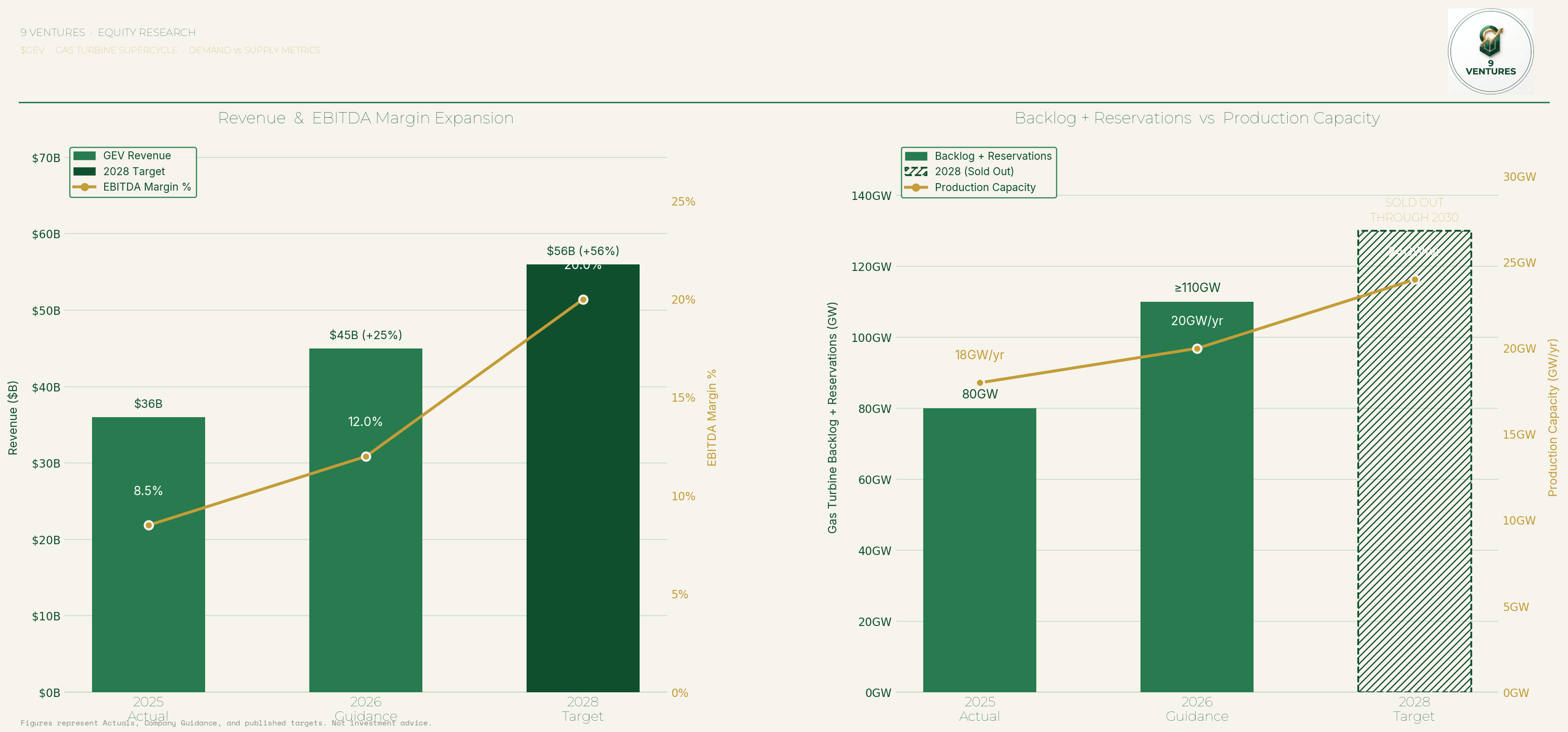

The OEMs are overwhelmed. GE Vernova, the dominant player in large gas turbines, entered Q1 2026 with 100GW in combined backlog and slot reservations, up from 83GW just the quarter before. $13B of new backlog added in a single quarter. CEO Strazik has said reservations will be sold out through 2030 by year-end 2026. They’re currently shipping at roughly 20GW/year. They cannot deliver 110GW in two years.

Siemens Energy is running the same playbook at greater scale. Their backlog just hit a new all-time high of €154B with a book-to-bill of 1.72x. In the first half of their fiscal 2026, they sold 179 gas turbines, nearly replicating all of fiscal 2025 in six months.

This is a supply chain event that spans most of the decade.

The Opportunity One Layer Below

Here’s what most people miss. Neither GE Vernova nor Siemens manufactures everything in-house. They depend on a network of qualified precision manufacturers embedded in their production processes, suppliers with the equipment, certifications, and institutional relationships that took decades to build and cannot be replicated quickly. These suppliers are the invisible infrastructure of the gas turbine supercycle.

The full deep-dive, including the specific name, ticker, segment-level analysis, margin progression, capacity utilization data, OEM relationship history, re-rating catalysts, valuation model, and price targets, is below.

NASDAQ: BWEN · Share Price ~$3.8 · Market Cap ~$88M

For informational purposes only. Not financial advice. Do your own due diligence. The author is long this stock.⚠️ LIQUIDITY DISCLOSURE — PLEASE READ BEFORE ACTING

This report covers a small cap security (~$88M market cap) with limited daily liquidity. If you read this research and determine $BWEN warrants a position in your portfolio, please be disciplined in your execution. Do not market buy. Use limit orders. Do not deploy a full position in a single session. Keep individual orders well below 10% of average daily volume. Aggressive buying in a thin market drives your own cost basis up. A patient entry matters as much as the thesis itself.

Broadwind ($BWEN) is a precision manufacturer with a six consecutive record quarters in its highest-margin segment, and 90%+ order growth YoY in its best quarter since 2022. It supplies the gas turbine supply chains of 4 of the top 10 global OEMs. It holds hardware that effectively does not exist anywhere else in the world. It has irreplaceable equipment and nearly a century of engineering expertise.

Broadwind has spent the last two years deliberately exiting a low-margin legacy business to concentrate entirely on the two segments now printing 40%-60% YoY growth.

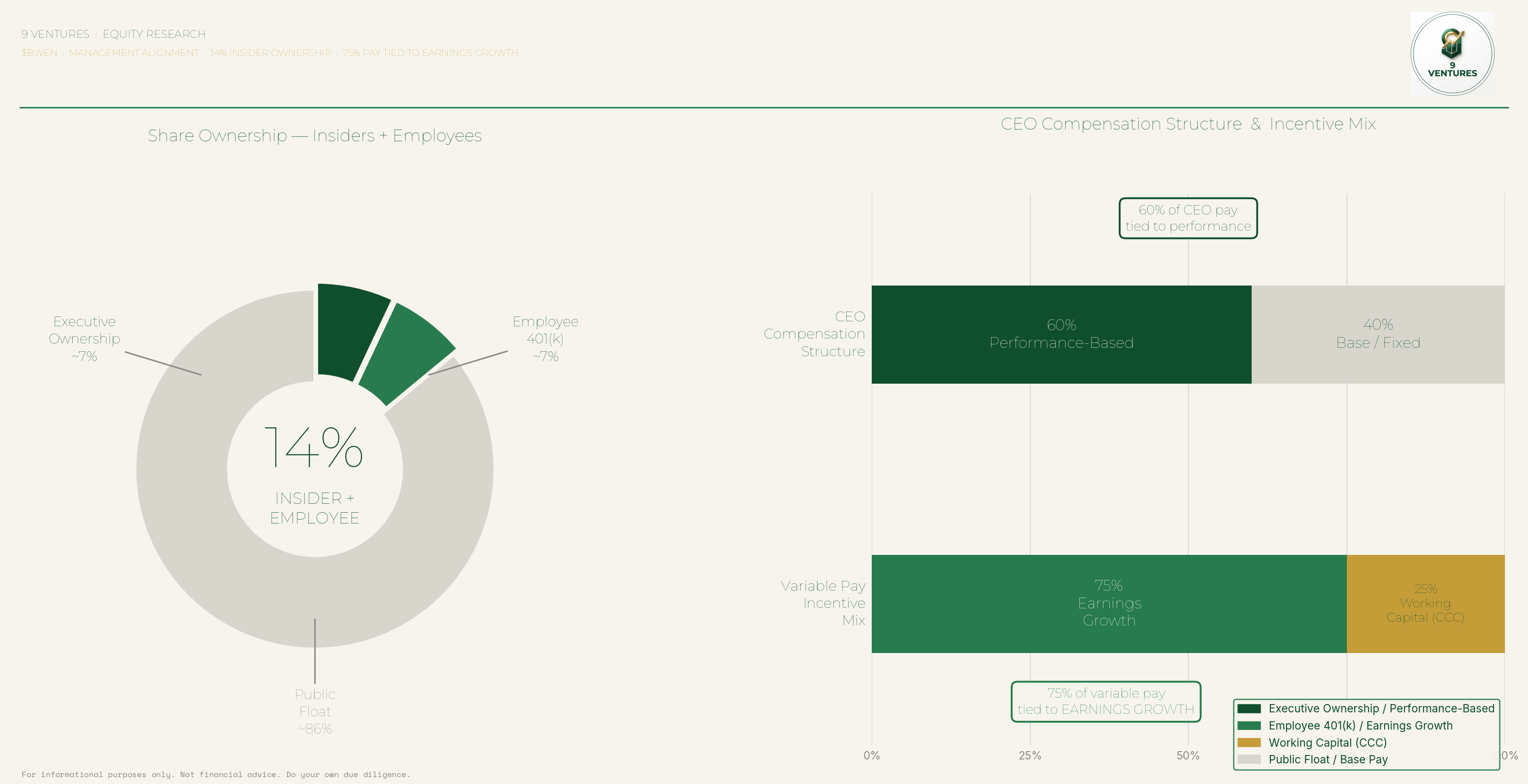

Management owns a 14% stake in the company. Their variable compensation is 75% tied to earnings growth. They are incentivized to make exactly the decisions they’ve been making.

00 — The Thesis

Power demand in the US has hit a level nobody in this industry was ready for. Gas turbines are by far the most popular behind-the-meter power solution right now, and $GEV and Siemens are already reporting 5-7 year lead times. OEMs are in full frenzy mode, prioritizing timelines and simplicity over everything else.

Broadwind is the overlooked precision manufacturer sitting in the middle of all this. They supply component kits directly embedded in the $GEV/$CAT/$ENR supply chain: precision gearing for gas turbines and outsourced kitting and assembly for natural gas turbine installations. They make rare, highly capable gears that enable higher rotational speeds, and they’re harvesting a weakening Wind Tower segment, cutting operating expenses and redeploying capital into the two segments that have real pricing power.

Combined backlog just hit $73M and growing. Industrial Solutions has set a record six consecutive quarters. Orders were up 90% YoY in their best quarter since 2022. Market cap is $90M.

A $90M micro-cap with a growing backlog, contractual OEM relationships, and irreplaceable manufacturing equipment, attached to one of the most powerful secular themes in public markets.

“While our exit from the Wind market will result in a smaller company over the near term, our remaining businesses are higher-growth, more predictable, and more profitable, with a meaningfully improved quality of earnings profile.”

— Eric Blashford, President & CEO, Q1 2026 Earnings

Check out this monthly base and this ignition volume last month!

01 — Industrial Solutions: Six Straight Record Backlogs

Revenue in Q1 2026 came in at $9.2M, up 64% year-over-year. $14.6M in new orders that quarter alone. Then April booked another $10M+ on top of that. Backlog hit a new record of $43.3M, more than $5M above the prior record set just the quarter before.

To understand why the IS position is defensible, you need one distinction: the “hot gas path” versus the “not hot gas path.” The hot gas path refers to components in direct contact with combustion gases at temperatures exceeding 1,000°C. Turbine blades, rotors, the core. These require exotic nickel superalloys, enormous R&D budgets, and are dominated by a handful of specialists.

Broadwind operates entirely outside this zone. CEO Blashford stated explicitly on the Q1 2026 call: “We tend to support those gas turbine installations on what’s called not hot gas path, but surrounding the hot gas path.” Valves, pumps, piping, heat exchangers, lubrication systems, generators, transformers, wiring harnesses, compressors, instrumentation, controls. Everything the turbine needs to actually run, manufactured from conventional materials at far better economics. A missing fuel valve stops the turbine just as effectively as a missing blade.

What makes IS specifically sticky is the service model wrapped around those components.

Pre-Testing. Broadwind pre-tests sub-assemblies before they leave the factory. For an OEM managing a complex installation timeline in an exponential demand environment, ready-to-install kits aren’t a convenience, they’re a requirement. Pre-testing integrates Broadwind deeper into the OEM workflow with every shipment.

Engineered Packaging and Sequencing. These kits are co-engineered with OEM teams: cable harnesses coiled for point-of-use installation, assemblies labeled for individual project specifications. Switching suppliers means rebuilding that co-engineered system from scratch. Nobody does that in a rush.

Just-In-Time Delivery. By aggregating components from multiple suppliers and holding them centrally, Broadwind lets OEM customers cut their own inventory carrying costs and eliminate stock-out risk. One partner, one purchase order.

“A leading global energy corporation sought a streamlined approach to procurement and supply chain management. It outsourced ALL aspects of its kitting container program to Broadwind Industrial Solutions, reducing storage needs and administrative costs. A single partner with a single purchase order.”

“Quote activity continues to increase in both Gearing and Industrial Solutions, generated by our ability to solve the complex precision manufacturing and sourcing challenges faced by customers in this growing market.”

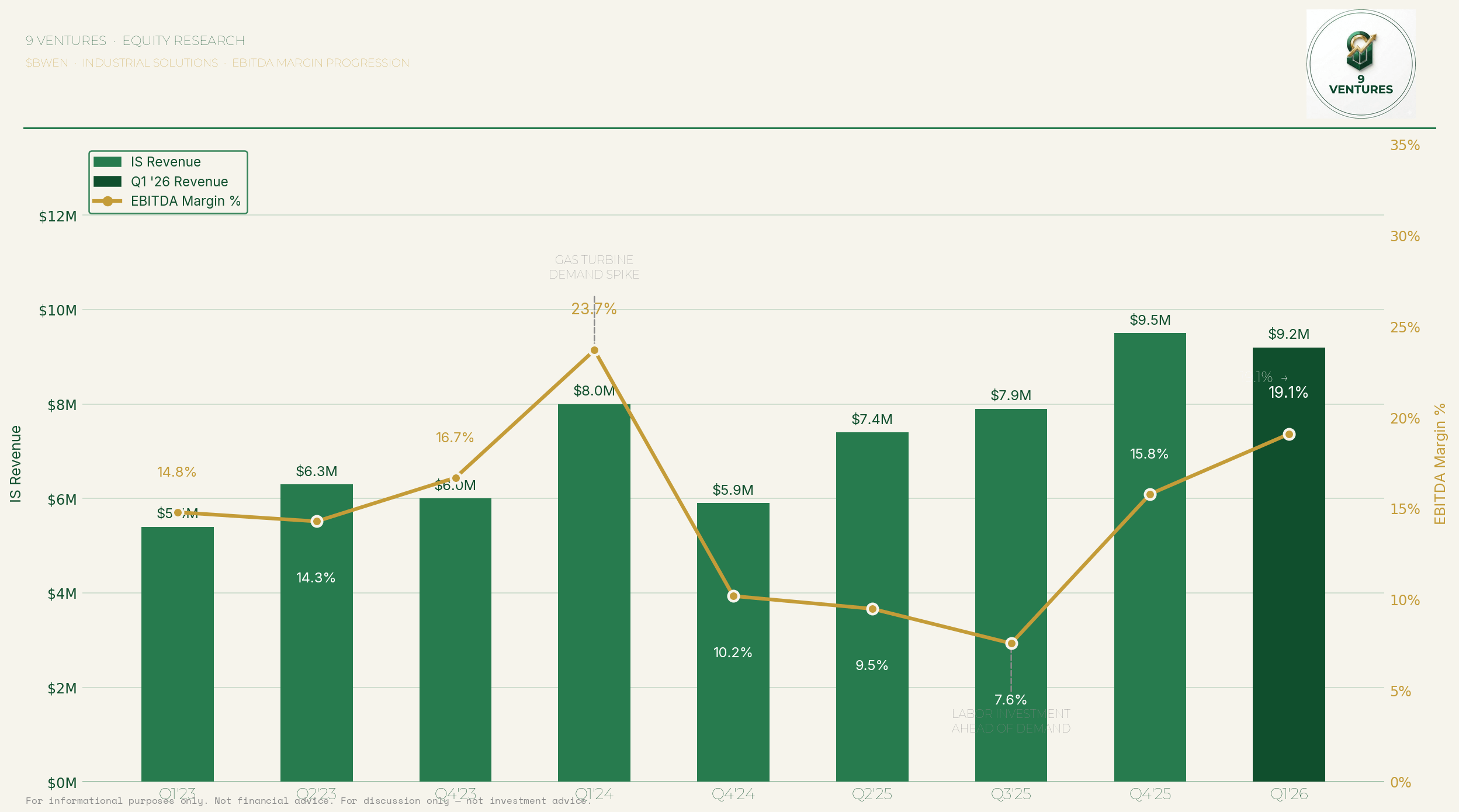

The margin progression tells the real story:

Margins went from 7.6% to 15.8% to 19.1% in two quarters while revenue was simultaneously growing. Operating leverage alone doesn’t do that. Broadwind cited increased labor costs in the mid-2025 dip, specifically flagging they were hiring ahead of the demand wave. Those costs have since been fully passed through to customers, which is the proof of pricing power, not just scale.

The Q1 2024 spike to 23.7% was attributed directly to “a major increase in demand for new and aftermarket gas turbines.” That’s the potential of this business when the cycle is fully firing. The current $43M backlog is concentrated in this segment. 20%+ IS EBITDA margins are a base case from here, not an optimistic scenario.

“Precision machining market remains very tight from a capacity standpoint as we look into the next several years.” — Eric Blashford, Q4 2025

02 — Gearing: The Technical Moat Nobody Is Talking About

Gearing is where the real moat lives. Brad Foote Gear Works engineers custom gearboxes and precision-machined components for aeroderivative gas turbines, high-torque power generation equipment, oil and gas processing, and aerospace and defense. Applications where failure has no tolerance.

Q3 2025 Gearing orders: $16M, up 260% YoY, the highest quarterly total in years. Inside that number was a $6M follow-on order from a leading gas turbine OEM, described as the minimum first-year commitment on a two-year agreement with potential for additional volume.

Why do 4 of the top 10 global gas turbine OEMs contract a micro-cap in Cicero, Illinois? The answer is irreplaceable hardware.

Brad Foote’s facility houses Gleason 675 Spiral Bevel Machines, two of four that exist worldwide, capable of machining AGMA 2000 Q10 gears up to 2.6 meters (104 inches). Gleason operates in a duopoly in the spiral bevel gear market, and these specific machines are no longer manufactured. A competitor cannot replicate this capability with capital alone. If an OEM needs a spiral bevel gear machined to AGMA Q10 at 104 inches, Broadwind is one of their only options, full stop.

It goes further. Broadwind built the largest climate-controlled grinding room in the U.S., housing 13 form tooth grinders, capable of producing gears to Q15 precision grade, the highest possible standard. Q15 requires climate control to minimize thermal expansion effects during grinding. Broadwind is a physical prerequisite for turbines running at the efficiency levels OEMs are promising their customers.

The GE relationship predates the current power hype by nearly two decades. In April 2008, Brad Foote signed a supply agreement with GE Transportation for wind turbine gearboxes. GE’s VP publicly stated that Brad Foote had “grown into a world class supplier to GE Transportation.” That institutional trust, built over more than 2,700 gear sets produced, is now being deployed on the gas turbine side. Broadwind also co-develops gearboxes with customers, optimizing design, manufacturing components, and performing internal testing before delivery. Structural integration, not transactional supply.

The capacity utilization lever. Management flagged on the Q3 2025 call that the Gearing facility was running at roughly 45% utilization. The business is booking orders at a pace unseen since 2022, and the factory is barely half-full. As utilization pushes toward 70-80%, fixed cost absorption improves dramatically. That lever hasn’t been pulled yet.

The proof is already in the numbers. Gearing went from -$0.3M EBITDA in Q4 2025 to +$0.6M EBITDA in Q1 2026, on a revenue increase of only $1.5M. That inflection on minimal revenue growth illustrates exactly how the fixed-cost math plays out from here. Management has guided for further operating leverage as utilization continues to climb, and a 100-year-old precision machining business with 4 of the top 10 global OEMs under contract is not a business that runs at 45% for long.

03 — Reading the OEM Scoreboard: $GEV and Siemens Are Booked Through 2030

Most people playing the power generation supercycle are buying $GEV or Siemens directly. That’s valid. BWEN is a different animal, a precision manufacturing supplier embedded in the OEM production process itself, one layer below the names everyone knows, at a fraction of the valuation.

GE Vernova. $GEV entered Q1 2026 with combined gas turbine backlog and slot reservations of 100GW, up from 83GW just the prior quarter. $13B of new backlog added in a single quarter. Targeting at least 110GW by year-end 2026. CEO Strazik has said reservations will be sold out through 2030 by end of this year. Currently shipping at roughly 20GW/year. They cannot deliver 110GW in two years. This is a supply chain event spanning most of the decade.

Siemens Energy. Similar story at greater scale. Backlog just hit a new all-time high of €154B with a book-to-bill of 1.72x. In fiscal 2025, Siemens sold 194 gas turbines total. In just the first half of fiscal 2026, they sold 179, nearly the full prior year’s volume in six months.

Neither GEV nor Siemens manufactures everything in-house. They depend on qualified precision manufacturers embedded in their supply chains. BWEN is one of those partners. When GEV adds 17GW to its backlog in a single quarter, BWEN starts receiving orders 6-18 months later. GEV’s backlog growth is a leading indicator for BWEN’s order flow, and that backlog is growing by $13B per quarter.

Three sequential orders illustrate the compounding relationship: Q1 2025 (largest gearing order to date), July 2025 (year one of a two-year LTSA with minimum volume commitment), and March 2026 (year two follow-on, same OEM). That’s a loyal customer under contract, not a transactional vendor relationship.

“Recent sizable orders we received from the power generation sector are the beginning of a multiyear cycle for which we are prepared.” — Eric Blashford, Q4 2025

04 — Book-to-Bill: The Cleanest Leading Indicator in Manufacturing

When a company consistently books more than it ships, backlog grows, forward revenue becomes visible, and revenues accelerate as capacity unlocks. BWEN’s two core segments have been running above 1.5x book-to-bill for multiple consecutive quarters.

Then April happened. $16M+ in new orders in a single month. $10M+ in Industrial Solutions. $6M+ in Gearing. This segment base is currently running at ~$75M annualized revenue. Converting that order rate comes down to manufacturing throughput, which is exactly why the North Carolina expansion and new Gearing equipment are the most important capital allocation decisions BWEN is making right now.

Clean precision manufacturers with similar profiles, sustained 1.5x+ book-to-bill, multi-year OEM agreements, 15-20%+ EBITDA margins, domestic manufacturing, trade at 14-18x EBITDA. BWEN’s implied multiple on core segment run-rate EBITDA is well below that band. When Q3 2026 is the first quarter reporting zero wind revenue, the street has no choice but to re-anchor the multiple to what this business actually is.

05 — The Wind Exit: Surgery, Not Triage

Blashford has been telling the same story consistently for two years. The actions match the words.

Manitowoc, Wisconsin — Sold September 2025. BWEN sold the Manitowoc industrial fabrication facility for $13M total consideration, generating an $8.2M net gain. The facility had generated over $25M in revenue in 2024 at roughly 8-9% EBITDA margin. Decent economics, but not compelling for a precision manufacturer moving upmarket. Management followed the sale with a $3M share repurchase authorization.

Abilene, Texas — Sold April 2026. The decisive move. BWEN sold the Abilene wind tower production facility to IES Infrastructure for up to $19.5M. In 2025, Abilene generated $56.3M in revenue and $9.7M in EBITDA. They walked away from nearly $10M of EBITDA to eliminate a business carrying single-customer concentration risk, federal tax credit dependency with a hard expiration at end of 2027, excess industry capacity creating price erosion, and the structural volatility of the domestic onshore wind market.

“Strategic exit from Wind market reduces exposure to regulatory, legislative, and business risk. In recent years, Broadwind’s wind-related revenue has been largely concentrated with one large wind OEM customer, while wind project economics have been largely dependent on federal tax incentives that will expire by year-end 2027.” — BWEN Press Release, May 2026

Both facilities were purchased by IES Holdings subsidiaries: Manitowoc in September 2025, Abilene in April 2026. A negotiated, structured exit to a single strategic counterparty who evaluated both assets deliberately. Clean.

The Abilene decision is counterintuitive on the surface. You’re selling a profitable business. But when Gearing and Industrial Solutions are growing at 40-60% per year and the remaining business has a century of precision machining expertise now clearing certification pathways into aerospace and defense, holding a fixed-cost wind factory serving one customer at the mercy of federal tax policy isn’t worth owning. Management’s compensation, 75% tied to earnings growth, makes their conviction on this clear.

“Despite the volatile trade policy environment, our 100% domestic manufacturing base remains a key competitive advantage positioning us to partner with tier one OEMs who value our deep technical expertise, commitment to quality, and on-time service.” — Eric Blashford, Q3 2025

06 — The Hidden Tax Asset: $300M in NOL Carryforwards

Almost nothing written about Broadwind mentions this. Broadwind carries nearly $300 million in net operating loss carryforwards, accumulated during years of wind business underperformance. At a 21% corporate tax rate, that’s approximately $63 million in future tax savings. For an $90M market cap company, that’s a material hidden asset sitting right on the balance sheet.

Management’s own press release stated: “Domestic acquisition strategy will seek to capitalize on nearly $300 million of net operating loss carryforwards.”

A company approaching profitability with $300M in NOL protection pays effectively zero federal income tax for the better part of a decade. Every dollar of EBITDA that converts to pre-tax income flows directly to the bottom line without a federal tax haircut. A rough NPV of that tax savings (spread out over a decade), discounted at 10%, adds $25-40M of value to the equity, or roughly $1.10 to $1.75 per share on a fully diluted basis. Most analysts won’t model it separately. It’s real regardless.

07 — Management Alignment: Skin in the Game

The incentive structure is what matters. 75% of variable compensation is tied to earnings growth, not revenue growth, not backlog growth. That alignment explains every capital allocation decision in this thesis: exit low-margin wind, concentrate resources in high-margin Gearing and IS, pursue LTSAs with earnings visibility, and clear certifications into higher-value markets. The remaining 25% tied to working capital management ensures the balance sheet discipline to execute without over-leveraging.

14% combined insider and employee ownership in a $90M micro-cap means the people making every decision in this thesis are personally invested in getting it right.

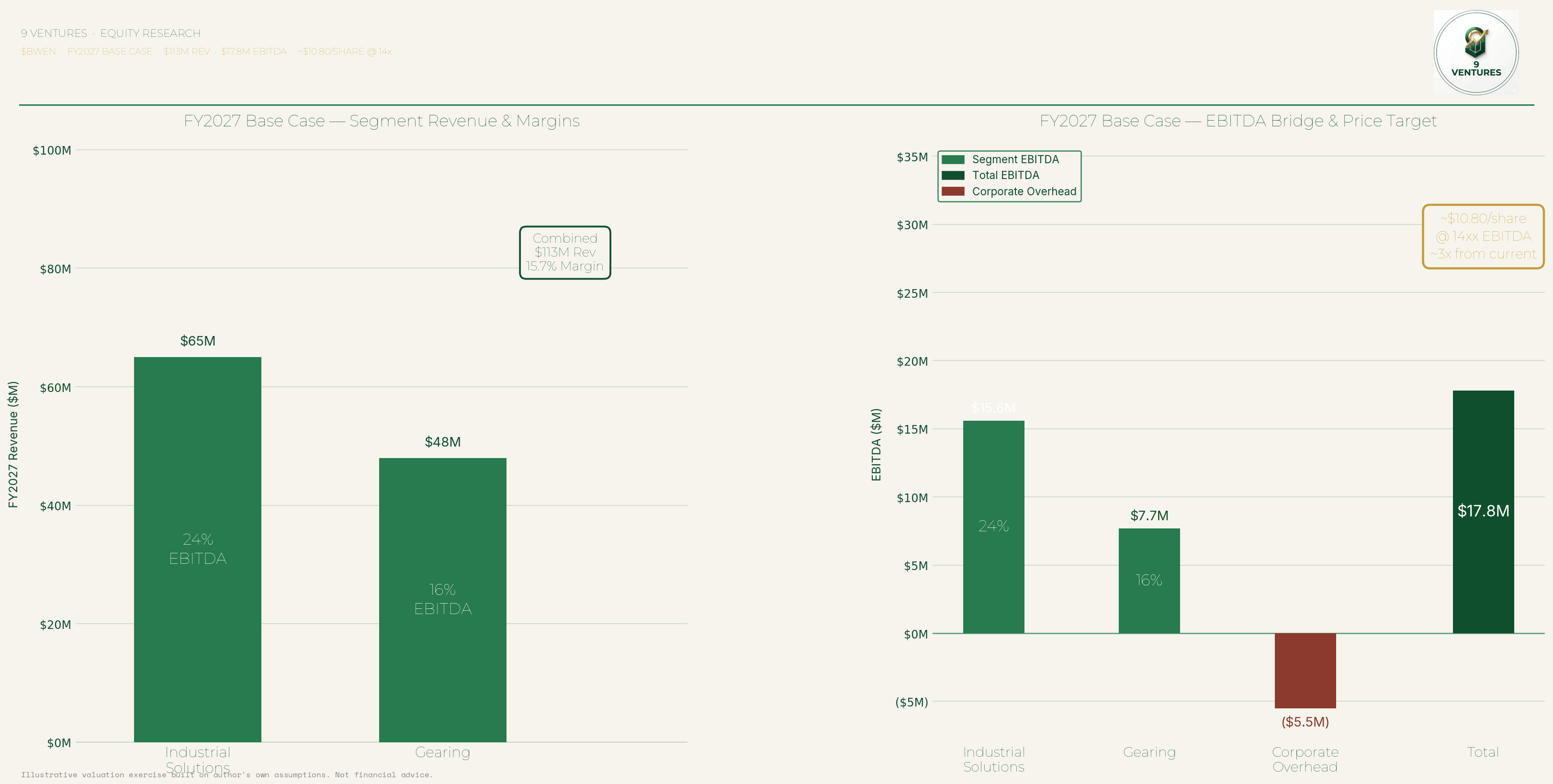

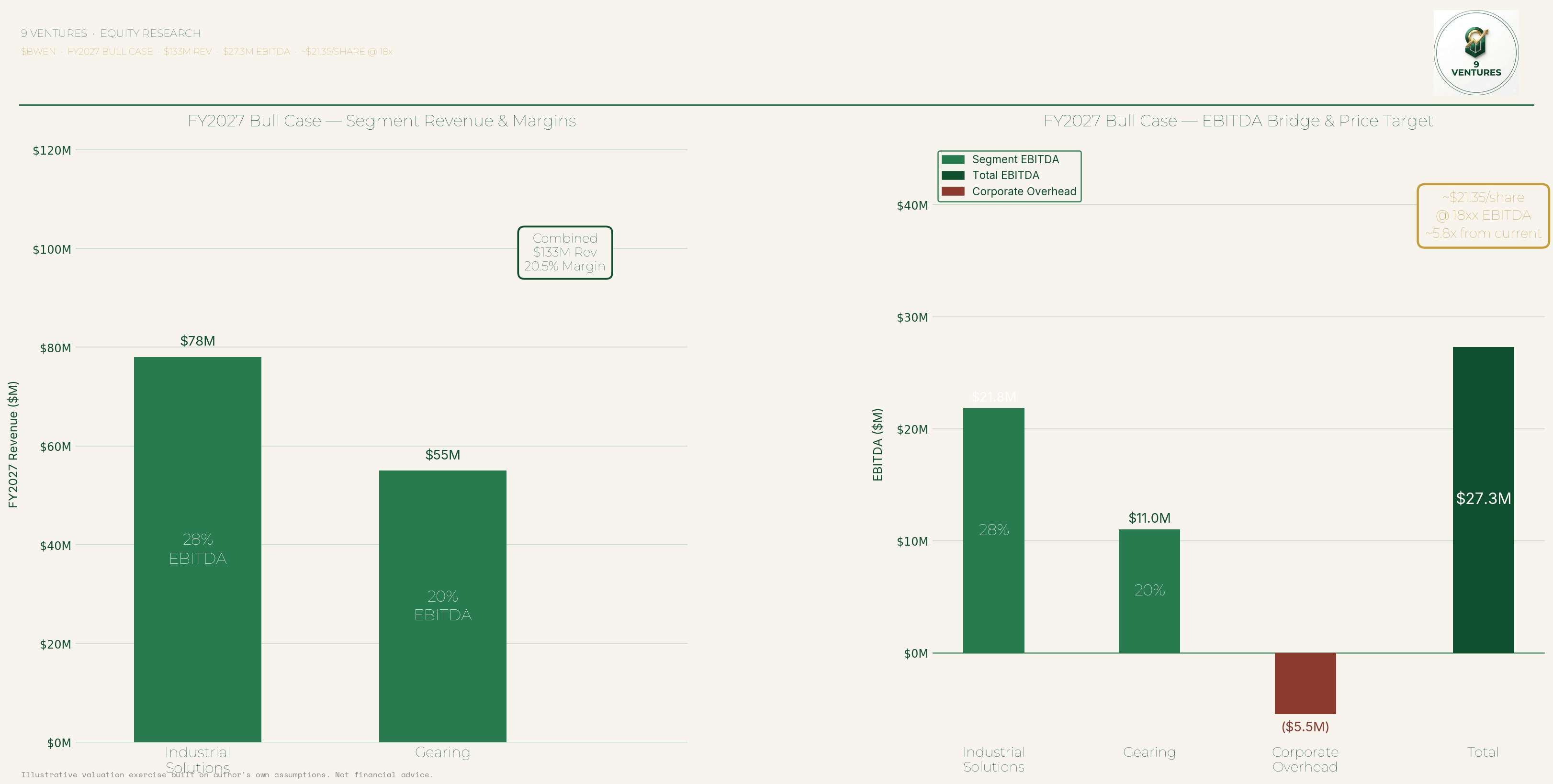

08 — The Model

Key Assumptions (FY2027): Industrial Solutions expands to $65-78M annualized revenue at 24-28% EBITDA margins. Gearing expands to $48-55M annualized revenue as utilization climbs from 45% to 70%+, producing 16-20% EBITDA margins from the fixed-cost base.

Base Case — FY2027

~$10.8/share at 14x EBITDA + $1.10 to $1.75 per share of PV tax savings = $11.9 - $12.55/share · ~$280M EV · ~3.3x from current levels

Bull Case — FY2027

~$21.4/share at 18x EBITDA + $1.10 to $1.75 per share of PV tax savings = $22.5 - $23.15 · ~$524M EV · ~6.1x from current levels

The 14-18x range is grounded in peer comps for clean pure-play precision manufacturers with 15-20%+ EBITDA margins, double-digit growth, multi-year OEM agreements, and direct exposure to the power generation supercycle. Post the Abilene sale, BWEN reports zero wind revenue. The street will eventually value the business on what remains, and what remains is very good.

Most would rather keep the NOL part separate, but for those interested, this math is how it (could) play out.

Additional Upside Case

A potential defense contract is likely given the DoD has only spent 17% of its newly awarded budget. Much of the budget is to be allocated to vehicles, weaponry, and other infrastructure, all of which require gears and have complex supply chains which could benefit from supply chain simplifiers. A multi-year contract at the least would fruit another $15-25M. These would likely be higher margin, at 30%+ EBITDA margins.

I expect BWEN to continue sustained 20%+ growth through FY30 given the backlog their customers face, implying a higher multiple than I have quoted above.

09 — Risks

Customer Concentration. Growth is driven by a small number of large OEM relationships. Switching costs on both sides provide protection, but the concentration risk is real and worth sizing around.

Execution During Transition. Running two divestitures while simultaneously scaling two fast-growing segments is operationally complex. Management has executed cleanly so far, but complexity compounds.

Gas Power Policy Risk. Any material policy shift slowing gas turbine permitting or penalizing natural gas generation is a headwind to both the OEM customers and BWEN’s order flow.

Micro-Cap Liquidity. $90M market cap means thin daily volume and wide bid-ask spreads. This is a position-sizing and patience game.

Guidance Withdrawal. BWEN pulled 2026 guidance when they announced the Abilene sale. Q2 2026 will be the first truly clean look at the core business without wind noise.

10 — Conclusion

$GEV is sold out through 2030. Siemens is booking 179 gas turbines in six months. The delivery ramp hasn’t even started. And sitting at $90M, with a $73M backlog growing every month, is the precision manufacturer kitting their turbines and machining their gears, with irreplaceable equipment, a 17-year OEM relationship, contractual minimum volume commitments, a defense certification stack being built in parallel, and a 30% expansion of North Carolina floor space coming in 2026.

$300M in tax-free earnings potential. A management team with 14% of the company and 75% of their variable pay tied to earnings growth.

This monthly base might just be the mother of all bases.

For informational purposes only. Not financial advice. Do your own due diligence. May 2026.

| A guest post by

|

a very well detailed report, really good stuff on the technicals of the business and the engineering side of it