Nebius Group: A Market Leader

Nebius ($NBIS) is the premier pure-play AI infrastructure company in the public markets. At a $38B market cap, the stock is severely undervalued. The market currently fails to account for its vertically integrated data center business and high-value specialized divisions.

The Neo-Cloud Data Center Business

The data center segment is the core of the Nebius investment thesis. Many competitors simply rent out GPU capacity. Nebius operates a vertically integrated AI infrastructure stack. The company controls every layer from hardware design to its proprietary Aether control plane. This software-first approach enables superior orchestration and higher GPU utilization rates.

Nebius prioritizes goodput over peak specifications. This ensures that customer workloads spend minimal time waiting for data. This technical edge allows the company to command a pricing premium for GPU capacity. A recent $2B investment from Nvidia ensures priority access to the latest Blackwell Ultra systems. The data center business is on a trajectory to reach between $7B and $9B in annual recurring revenue by the end of 2026.

Strategic Stakes and Ecosystem

The Sum of the Parts valuation is bolstered by several high-growth specialized divisions.

• ClickHouse: Nebius holds a 25% stake in this high-performance database leader. ClickHouse uses a unique architecture for real-time analytics. This stake alone could be worth $10B to $15B as demand for real-time AI data processing scales.

• Avride: The autonomous driving division is working with Uber to deploy robotaxis. This partnership validates the software stack. It provides a clear path to commercialization in the physical AI space.

• Toloka and TripleTen: Toloka provides the human-in-the-loop alignment layer for Large Language Models. TripleTen serves as the educational pipeline for the next generation of engineers.

• Tavily: The recent acquisition of this agentic search company enhances platform capabilities for the agentic AI era.

Financial Health and Capital Structure

Nebius maintains a much stronger balance sheet than its primary neo-cloud peers. Competitors often rely on extreme leverage to fund capital expenditures. Nebius prioritizes a sustainable debt-to-asset ratio.

The $4B convertible senior note offering in March 2026 was upsized due to high demand. This successful raise placed the convertible overhang in the rear view. The notes were issued at a conversion premium of over 55% relative to the share price of $116.33. This structure provides the necessary runway for global expansion while minimizing immediate dilution. The company is now fully funded to build out its planned 5 GW of capacity by 2030. Management has a clear line of sight to reach $40B in annual recurring revenue from the data center business by that time.

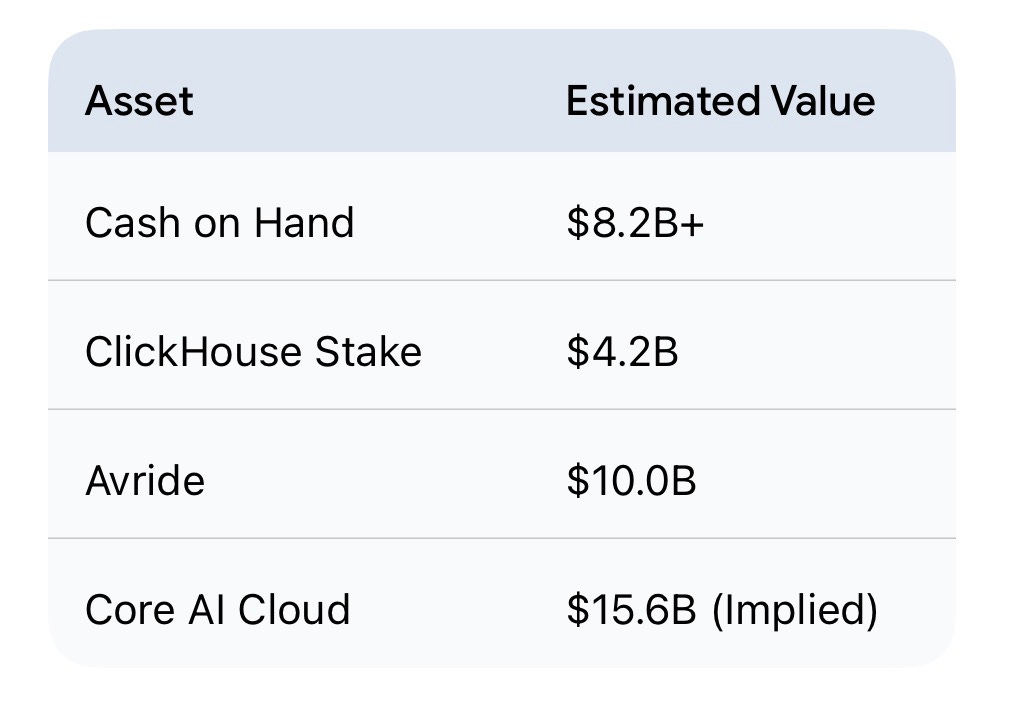

The Asset Math

Nebius is fundamentally mispriced at its current valuation. The market is ignoring high-value subsidiaries and significant emerging operating leverage. According to Yahoo Finance, the current market cap stands at $38B.

The core AI infrastructure business is currently trading at a deep discount.

• Scale: Reaching $8B ARR midpoint by year-end 2026.

• FY27 Outlook: Estimated $12B in revenue.

• Profitability: Trading at less than 10x FY27 EBITDA.

If we strip out the $15B in subsidiary value, the core business trades closer to 5x FY27 EBITDA and 1.25x FY27 sales.

Conclusion

A $60B market cap is the floor for a business with this growth profile. Nebius is one of the only neo-cloud providers that is not over-leveraged. At the current $38B valuation, the stock represents a significant opportunity.