$NVTS: The 800V Architecture Pure Play

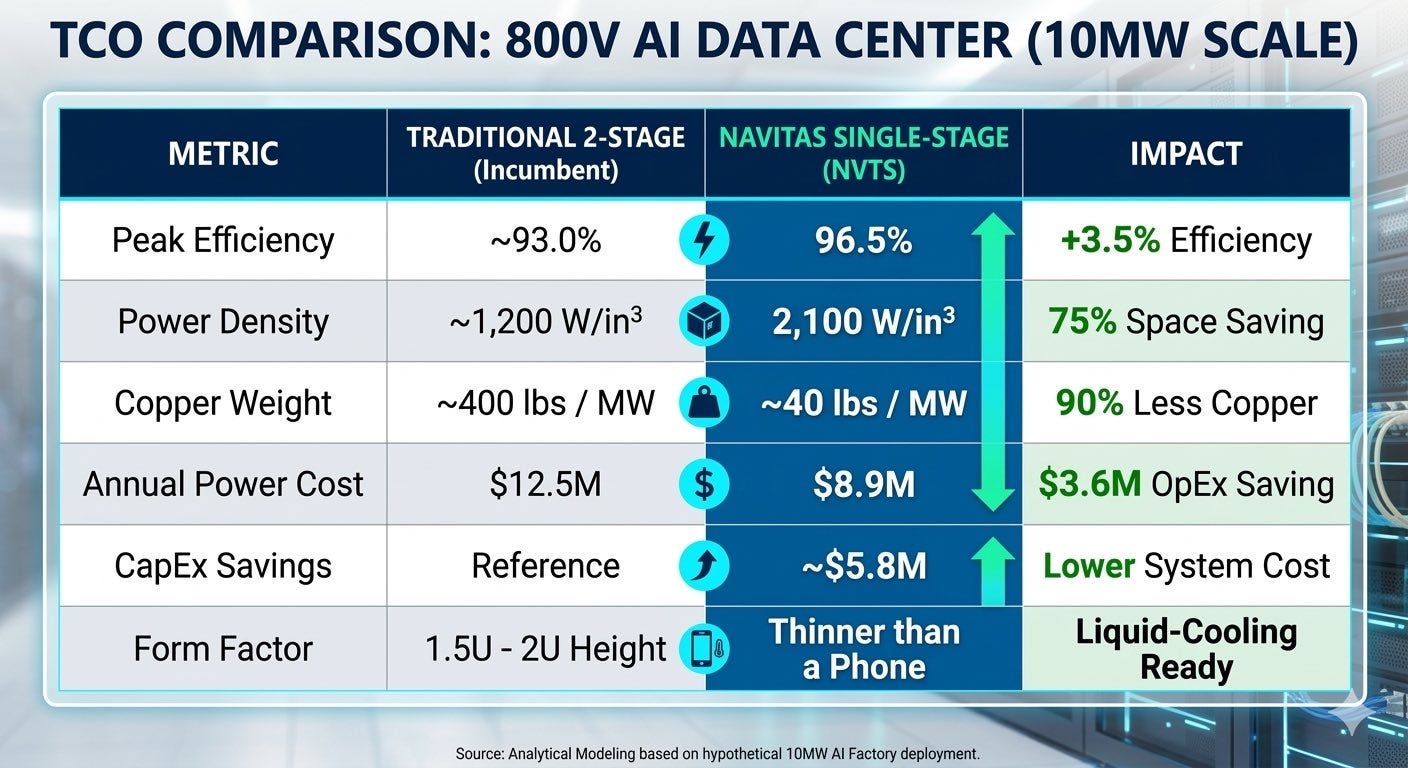

The Navitas $NVTS 800V-to-6V DC-DC power delivery board represents a fundamental departure from traditional server power design. Most current data centers utilize a two-stage conversion process. This legacy system steps 800V down to an intermediate 48V bus before a second conversion reaches the low-voltage rails for the GPU.

Navitas eliminates the Intermediate Bus Converter entirely. This single-stage approach achieves several critical system-level objectives:

Removing the 48V IBC frees up valuable physical space on the server tray. This allows for higher density of HBM and compute silicon. Stepping down from 800V directly to 6V halves the conversion ratio for the final Voltage Regulator Modules. This reduces the electrical stress on point-of-load components and improves thermal performance. The board delivers 2,100W per cubic inch. Its profile is approximately 20% thinner than a mobile phone. This form factor is essential for the vertically-mounted "blade designs in the upcoming Kyber rack architecture.

The transition to 800VDC (High Voltage DC) is a requirement for the next generation of accelerated compute. As rack power requirements approach 1MW for the Vera Rubin and Blackwell Ultra platforms, traditional 48V distribution becomes physically impractical due to extreme copper requirements and resistive losses. Navitas aligns directly with NVIDIA’s 800VDC roadmap. By converting power at the tray level with 96.5% peak efficiency, Navitas minimizes heat generation within the dense compute fabric. This efficiency gain is critical for liquid-cooled environments where thermal overhead is the primary constraint on performance scaling.

Navitas currently holds a first-mover advantage in the single-stage 800V-to-6V category. Established competitors like Vicor $VICR and Monolithic Power Systems $MPWR primarily focus on stepping 800V down to a 48V or 54V rail to maintain compatibility with legacy components.

The competitive moat for Navitas rests on two pillars:

1. The board utilizes sixteen 650V GaNFast FETs in a stacked full-bridge configuration. This integration allows for a 1MHz switching frequency, which significantly reduces the size of passive components like inductors and capacitors.

2. If NVIDIA adopts the 6V output as a reference design for their architecture, competitors must redesign their entire power portfolios to match this single-stage conversion path.

The Navitas 800V-to-6V solution is a key enabler for the Kyber rack generation. It addresses the physical and thermal limitations of the 48V bus while providing the power density required for 1MW AI factories. This development positions Navitas as a critical vendor for the next phase of hyperscale infrastructure build-outs.

I've also leveraged Gemini to help me show the potential TCO difference between incumbents and $NVTS. Gemini helped me devise the above also. Would love to hear people's opinions or counter arguments.

I studied Navitas like a month ago. The main issue I see with it is that their architecture has to be chosen by Nvidia in order for them to have the competitive advantage. If, for whatever reason, that 1 stage voltage reduction ends up not working as expected and a 2 stage voltage transformation is finally adopted, their competitors will eat their lunch. If their arquitecture is chosen, they have the advantage, but we don’t know for how long.

When analysing the metrics of the company, much of the future sales are already anticipated in their market cap. I did some models with the help of chatgpt and, taking into account the guidance given by the management in their company presentation (25 - 35 kUSD / MW), they would have to sell to approximately 5GW of power at 50k USD/MW (250M USD of revenue) and with a P/S of 10 to have a market cap of 2.500 M USD, which is a bit less than their current market cap. Notice that 5GW is a lot of power to feed and that I am using a price/MW higher than the one given by the management. Management may be sandbagging, but it’s worth taking that into account.

I understand that the technology looks attractive and that it may be a breakthrough, but much of the future growth is already anticipated in the stock price. This is why I didn’t take a position in the end in the company.

Hope this information was useful.